Reading the Tells

The architecture is being staged in plain sight. Two signals indicate whether the trigger conditions are approaching. Both are public. Most analysts don’t know what to look for.

The first is Federal Reserve posture. The Federal Reserve runs U.S. monetary policy through three main instruments: short-term interest rates, the size and composition of its balance sheet (the trillions in Treasury bonds and mortgage-backed securities it holds), and forward guidance about what it will do next. For most of the post-2008 period, all three instruments have been deployed to keep money cheap and asset prices high. That regime is the suppression the BlitzCorrection thesis depends on lifting.

The second is insider distribution. Specifically, the legally required disclosures of stock sales by senior executives, directors, and major shareholders that document elite selling into the mechanical passive bid. Both signals are leading indicators of trigger readiness. Reading them does not produce a date. Reading them indicates whether the architecture is positioned for the trigger event when conditions provide it.

The Fed posture

The Federal Reserve and the Treasury Department are not the same institution. Treasury is part of the executive branch and answers to the President. The Fed is statutorily independent and answers in theory only to its dual mandate of price stability and maximum employment. For most of the post-2008 period the two have been functionally aligned: both supporting the suppression that produced the rentier coalition’s margin structure. The Genesis Architecture changes that alignment.

Treasury Secretary Scott Bessent has called the post-2008 monetary regime “gain-of-function” monetary policy. The phrase is technical but the meaning is clear. What the Fed has been doing since 2008 is amplifying the risk concentration in the existing financial architecture rather than allowing the market mechanisms that would normally redistribute it. Bessent describes this as an instrument rather than a problem. The instrument has produced specific outcomes the architects now want to redirect.

To understand what redirecting means: when prices fall sharply, suppression is the set of Fed actions that keeps prices from falling at the speed the market would otherwise produce. The Fed cuts rates to make borrowing cheaper. The Fed buys bonds to push their prices up and yields down. The Fed signals through forward guidance that it stands ready to do more. The result is that even when sellers heavily outnumber buyers, suppression provides Fed-supported demand so prices don’t actually fall. Letting velocity run means stepping back from those interventions and allowing the natural compression to happen at the speed the algorithmic plumbing of the modern equity market produces.

Treasury wants velocity. The architecture needs the discrete repricing event that velocity produces. Suppression is the mechanism that has prevented it for fifteen years.

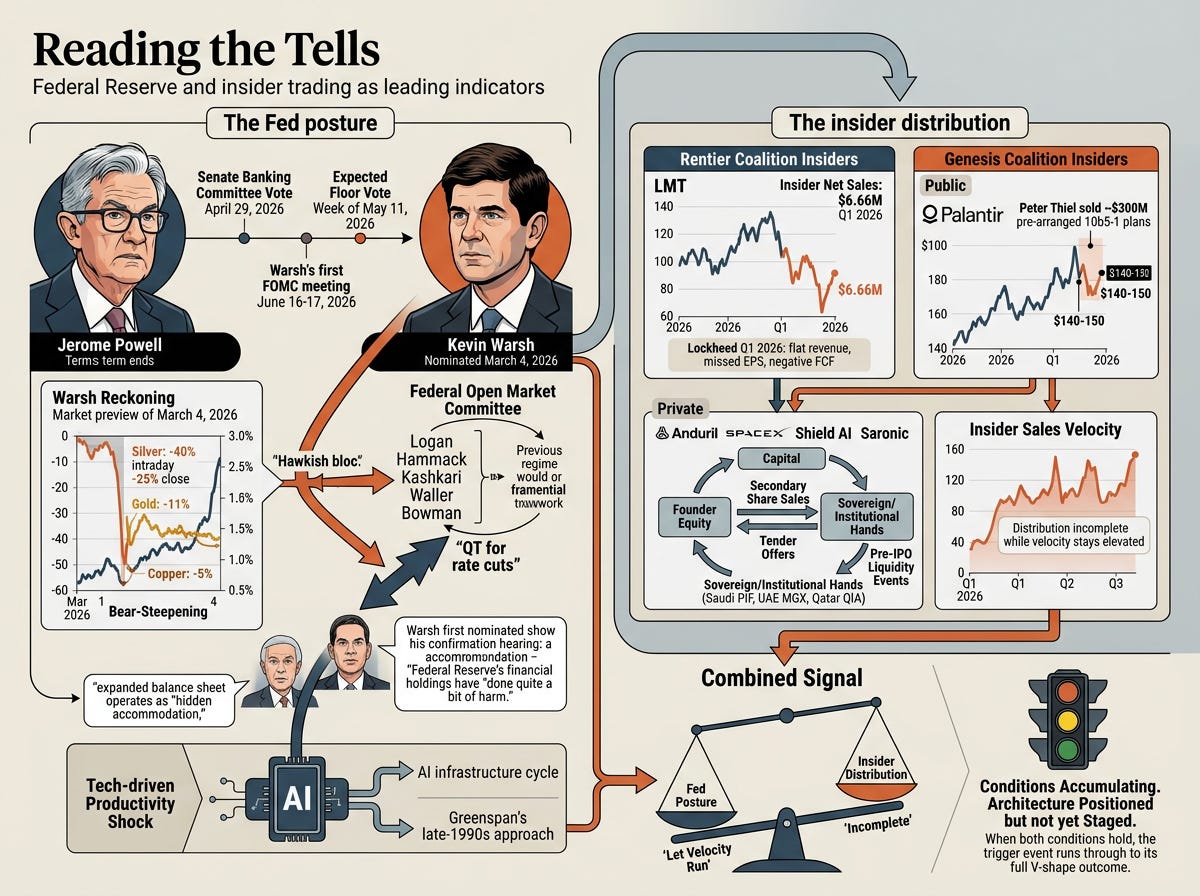

The institutional resolution of the Treasury-Fed alignment problem is now happening through a personnel change. Jerome Powell’s term as Fed Chair ends May 15, 2026. President Trump nominated Kevin Warsh to succeed him on March 4, 2026. The Senate Banking Committee voted 13-11 along party lines to advance the nomination on April 29, 2026. The floor vote is expected the week of May 11. Warsh’s first FOMC meeting as Chair is scheduled for June 16-17, 2026.

Warsh’s record demonstrates a long-standing public critique of exactly the suppression regime Bessent now wants to roll back. Warsh served on the Federal Reserve Board from 2006 to 2011 and has spent the fifteen years since as a Hoover Institution affiliate writing and speaking about the distortive effects of the post-2008 monetary architecture. His positions are documented in writings, congressional testimony, and public statements that span multiple administrations.

The summary of what Warsh has said: the Fed’s expanded balance sheet operates as “hidden accommodation” that benefits asset holders, distorts capital allocation, and removes price discovery from the private sector. During his April 21, 2026 confirmation hearing before the Senate Banking Committee, Warsh testified that the Federal Reserve’s financial holdings have “done quite a bit of harm” to the institution’s overarching credibility. He has called for a new Treasury-Fed Accord modeled on the 1951 agreement that formally separated debt management from monetary policy, this time aimed at binding the central bank to a smaller balance sheet and a narrower mandate.

Warsh’s critique is structurally identical to Bessent’s gain-of-function framing. The two diagnose the same problem and prescribe the same solution: the Fed should retreat from its post-2008 expansion, allow market mechanisms to reassert themselves, and accept that asset price corrections are part of normal market function rather than crises requiring intervention.

The market got a preview of what Warsh-led Fed posture looks like in the days after his March 4 nomination announcement. Institutional analysts called the event the “Warsh Reckoning”. Yields on long-dated Treasuries rose sharply as investors priced in the expectation that Warsh would step back from the Fed’s role as buyer of last resort for the long end of the curve. The yield curve “bear-steepened,” meaning short rates held while long rates rose. Risk assets repriced violently. Silver futures fell nearly 40% intraday before closing down 25%. Gold fell 11%. Copper fell 5%. Leveraged exchange-traded funds and speculative instruments dumped into the suddenly illiquid environment to rebalance their exposure.

Warsh said nothing publicly during the repricing. He did not signal Fed intervention. No reassurance came from his office. The move was framed neither as orderly nor as a crisis. He let it happen.

That silence is the preview. The Federal Reserve under Warsh will not reflexively defend asset prices when velocity arrives. The architecture’s preferred Fed Chair behavior, letting the compression run rather than suppressing it, is the behavior the market just observed in compressed form during the Warsh Reckoning.

But the institutional picture is more complicated than personnel change alone resolves.

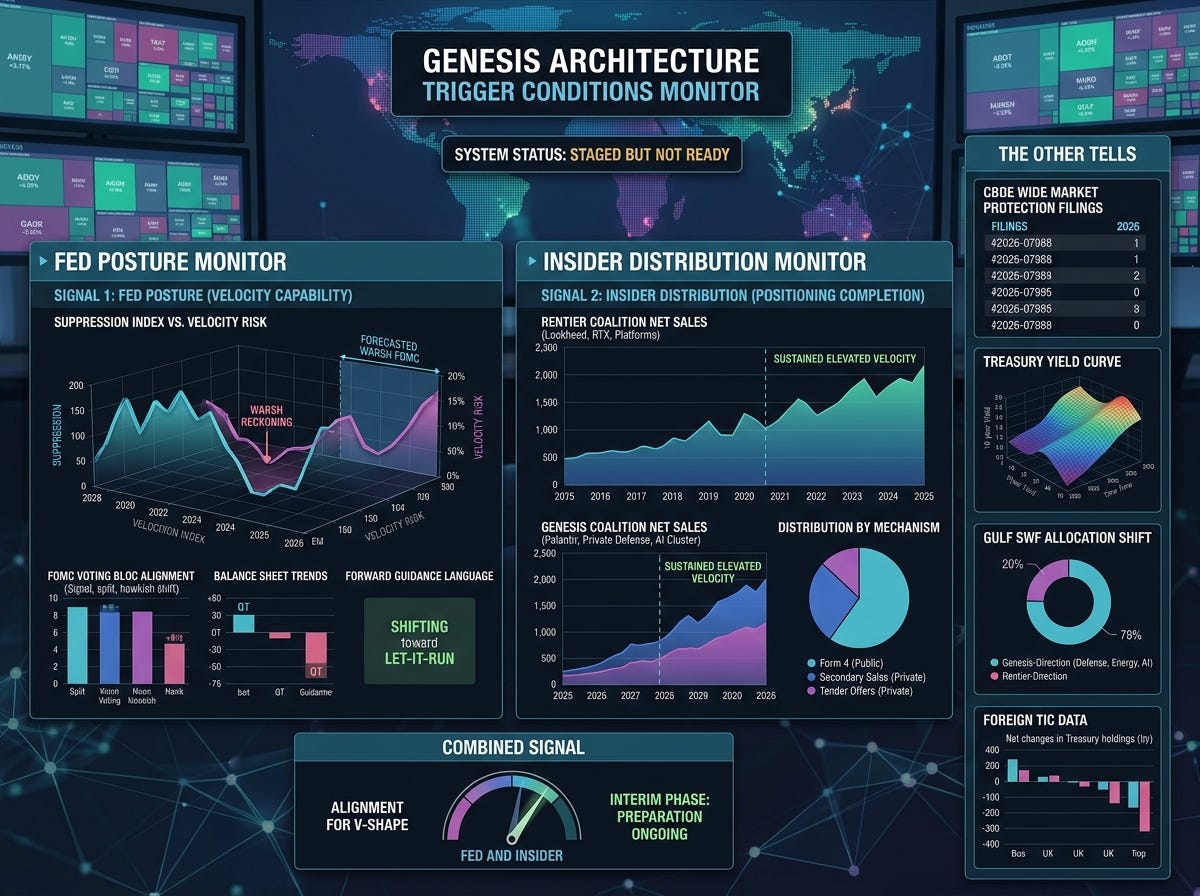

The Federal Open Market Committee, the body that actually votes on Fed policy decisions, consists of the seven Board of Governors plus the New York Fed President and four rotating regional Reserve Bank presidents. Warsh inherits a committee defined by deep internal division. The April 28-29, 2026 FOMC meeting (Powell’s last as Chair) produced four dissenting votes, the highest number at a single meeting since October 1992. The 2026 rotation brought a hawkish bloc to the voting table: Lorie Logan of the Dallas Fed, Beth Hammack of the Cleveland Fed, and Neel Kashkari of the Minneapolis Fed are all identified by institutional analysts as “very hawkish.” Christopher Waller and Michelle Bowman on the Board of Governors are also hawkish. They will resist aggressive interest rate cuts and may resist the specific framework Warsh has articulated, called “QT for rate cuts,” in which lower short-term rates are paired with continued or accelerated balance sheet shrinkage to keep overall financial conditions neutral.

Powell himself plans to remain on the Fed Board as a sitting Governor after his Chair term ends, the first time since 1948 that a former Chair has done so. He cited the need to defend the institution’s independence from administration pressure. By staying, Powell denies the administration the immediate appointment of another loyalist Governor and creates what institutional analysts have called an alternate center of power within the Fed.

Warsh also brings a specific view of the AI infrastructure cycle that matters for the apex earnings question covered in earlier pieces. He has explicitly framed the AI buildout as productive supply-side investment rather than speculative excess. In Senate testimony he characterized AI as American ingenuity that gives the U.S. a substantial head start over global competitors and predicted that what is currently called artificial intelligence will be viewed as ordinary business CapEx within two years. He models his framework on Alan Greenspan’s late-1990s approach: a technology-driven productivity shock allows higher growth without inflationary pressure, which justifies lower short-term rates over the medium term. Translation for the BlitzCorrection thesis: a Warsh-led Fed will not view multiple compression at the hyperscaler apex as a crisis warranting defensive intervention. He sees the underlying CapEx as real, the productivity gains as real, and the multiple compression as appropriate market repricing rather than threat.

The result: Warsh’s chairmanship is likely to produce institutional change at the margins rather than dramatic immediate transformation. Warsh wants a sweeping liquidity reset. The institutional structure of the FOMC will moderate that ambition. The shift in Fed posture toward letting velocity run is real but slower than Bessent’s framework would prefer.

The leading indicator for this slower shift: Warsh’s first FOMC minutes after his June 16-17 meeting. Specifically the language on financial stability, asset prices, and the relationship between rate cuts and balance sheet management. When the minutes describe sharp asset-price moves as necessary repricing rather than elevated valuation pressures requiring intervention, the institutional alignment with Treasury preference has shifted. Until that language changes, the Fed remains a partial friction in the architecture’s preferred timing. Softer friction than under Powell, but friction.

The insider distribution

The personal-wealth-extraction behavior of the architects is documented in real time on SEC EDGAR. Anyone with internet access and the patience to read Form 4 filings can watch the distribution happen. Most analysts don’t bother. The filings are public, dated, and signed.

Form 4 is the Securities and Exchange Commission’s required disclosure form. Senior officers, directors, and shareholders owning more than 10% of a public company’s stock must file a Form 4 within two business days of any transaction in their company’s shares. The form reports the date, the share quantity, the price, and the type of transaction. Most large insider sales are executed under what’s called a 10b5-1 plan, a pre-arranged automatic selling schedule that the executive establishes months or quarters in advance. The advantage of a 10b5-1 plan for the insider is that it provides a legal defense against claims of insider trading, because the sales are scheduled before the executive could have known about the specific events affecting the share price on the sale date. The advantage for the architecture is that it allows scheduled distribution into a market that absorbs the supply through the mechanical passive bid.

Two patterns matter.

The first is the rentier coalition insiders. Lockheed Martin, RTX, Northrop Grumman, the platform monopolies, the pharma-PBM oligopoly. When senior officers and directors of these firms file 10b5-1-scheduled sales at sustained elevated rates, they are exiting positions ahead of the multiple compression they expect to come. Lockheed Martin’s Q1 2026 earnings reported flat year-over-year revenue, missed EPS, and negative free cash flow of $291 million. Insider net sales totaled $6.66 million over the 90-day window ending in May. That number is not catastrophic on its own. Sustained over three or four consecutive quarters at elevated rates, it becomes a pattern that says: management does not believe the multiples will hold.

The second pattern is the Genesis Coalition insiders. These are the sales that matter more, because Genesis insiders know the rotation timing from the inside in ways rentier insiders do not. The mechanics are different depending on whether the company is public or private.

For public Genesis Coalition companies, with Palantir as the cleanest example, the mechanism mirrors the rentier-coalition mechanism. Form 4 filings, 10b5-1 plans, scheduled sales into the public market. Peter Thiel sold approximately $300 million worth of Palantir shares between late 2025 and mid-2026 via pre-arranged 10b5-1 plans. CEO Alex Karp, CFO David Glazer, and Director Alexander Moore liquidated heavy tranches at $140-150 per share through the same instruments. The sales are documented on EDGAR. Anyone can read them.

For private Genesis Coalition companies (Anduril, SpaceX, Shield AI, Saronic, and the rest of the privately-held Defense-Industrial 2.0 cluster), there is no public stock. The shares are held by founders, early employees, early venture capital investors, and sovereign limited partners who came in through funding rounds. Insiders cannot simply sell on the open market because there is no open market for the shares. So they extract cash through three mechanisms that produce the same economic effect.

Some Genesis Bipartisanship from everyone’s favorite F Bomb dropper:

Secondary share sales: an existing shareholder sells privately-held shares to a new investor at a privately-negotiated price. This typically happens between formal funding rounds. The transaction is reported to the company and may show up in Delaware corporate filings or in tender offer documents, but it does not produce a Form 4 because the company is private.

Tender offers: the company orchestrates a buyback program that allows insiders, including founders, early employees, and early investors, to sell a specified portion of their holdings at a set price, often timed in conjunction with a new funding round. New money comes into the company at a high valuation while existing shareholders extract cash at the same valuation. Anduril’s reported valuation move from $30.5 billion in June 2025 to a $60 billion target in March 2026 likely involved tender offer mechanics that allowed founder equity to exit partially while sovereign wealth funds and institutional investors entered at the higher valuation.

Pre-IPO liquidity events: founders convert illiquid private equity to cash through one of several private market structures before the company files for a public offering. The mechanics vary but the economic effect is the same: insider cash extraction at peak private valuations, with sovereign or institutional buyers absorbing the shares at first-mover entry prices that retail investors cannot access.

The phrase “founder equity rotating to sovereign or institutional hands at favorable valuations” describes this entire pattern. The valuations are favorable to the buyers (Saudi PIF, UAE MGX, Qatar QIA, the major sovereign wealth funds) because they get in at private valuations that are high but represent first-mover positioning before any IPO repricing. The valuations are also favorable to the founders, because they extract cash at peak private valuations before the public market gets a chance to discipline the multiple. Both sides are positioning ahead of the rotation. Both sides are extracting value that the public-market retail investor will never have access to at those terms

.

The tell across both public and private mechanisms is velocity. While insider sales velocity stays elevated, measured across Form 4 filings for public companies and across observable tender offer or secondary sale activity for private companies, distribution is incomplete. While distribution is incomplete, the architecture is not ready. When sales velocity drops sharply across both rentier and Genesis insiders simultaneously, the distribution phase is approaching its end. That is the signal that the architecture has cleared its insider-positioning precondition.

Q1 2026 sales velocity was high. Q2 2026 looks similar based on early filings. The pattern continues.

Reading the velocity

The structural read on these signals depends on understanding what the velocity actually represents.

Insider sales reflect operating-fundamentals knowledge that external analysts cannot model. The sales are positioning based on internal information about the firm’s revenue trajectory, customer concentration, and competitive moat. When Karp and Glazer file simultaneous tranches at $145 per share through 10b5-1, they are signaling that the share price reflects assumptions about Palantir’s revenue trajectory and competitive moat that they believe are too optimistic to hold. The signal is about valuation, not market timing.

The same logic runs through Lockheed insider sales. Q1 2026 printed flat year-over-year revenue, missed EPS, and negative free cash flow. Senior insiders see the operating pipeline more clearly than analysts can model. When they sell into the passive bid at sustained pace, they are exiting at multiples they consider unsustainable.

Reading the velocity is reading the pattern across many filings simultaneously. A single insider sale signals little. Sustained elevated velocity across many insiders at many firms in both factional categories indicates the architecture is in distribution. Declining velocity at the same scope indicates distribution is approaching completion. The transition from elevated to declining is the signal.

The transition has not happened yet as of this writing.

The combined signal

Fed posture and insider distribution are both necessary conditions for the trigger event. Neither alone is sufficient.

If the Fed continues suppressing while insiders distribute, the architecture cannot fire because the suppression keeps the bid under the legacy positions even as elite capital exits. The exit liquidity is provided by the passive bid, but the no-bid event requires the suppression to lift. The Fed has to step back from defensive intervention for the velocity to run.

If the Fed lifts suppression while insider distribution remains incomplete, the architects don’t get the V-shape they need. The compression starts before elite capital has finished exiting. Insiders take losses on positions they had not yet liquidated. The political coalition that funded the architecture loses its primary backers’ confidence. The rotation fails politically before it completes structurally.

Both conditions have to align. The Warsh Reckoning of March 2026 demonstrated that under a Warsh chairmanship the Fed will not reflexively defend asset prices during velocity events. That tilts the Fed posture variable toward architecture alignment. The institutional moderation of the FOMC means the alignment is partial rather than complete in the near term. Distribution remains incomplete based on Q1 and Q2 2026 insider sale velocity. When both conditions hold, with Warsh having consolidated FOMC support for the let-it-run posture and insider sale velocity having dropped sharply across both factions, the architecture is staged. The trigger event that arrives next, whether from Iran or apex earnings or some other source, runs through to its full V-shape outcome rather than being suppressed or aborted.

The signal density on both variables is what makes them readable. The Fed posts FOMC minutes after every meeting. SEC EDGAR updates daily. Tracking both does not require special access. It requires knowing what to track.

The other tells

Several other indicators run alongside Fed posture and insider distribution. None is as load-bearing, but each adds to the readability.

Cboe Wide Market Protection filings. Cboe Global Markets operates several U.S. equity and options exchanges including BZX, EDGX, and the C2 Options Exchange. In April 2026, Cboe filed proposals with the Securities and Exchange Commission for what it called Wide Market Protection mechanisms. The filings asked the SEC to approve a specific set of circuit breakers, trading halts, and alternative routing protocols designed to handle scenarios in which simultaneous stop-loss orders triggered by sharp price moves exhaust available liquidity. In plain English, the exchanges asked for permission to install kill-switches in case prices gap so violently that there are no buyers on the other side of the trades. The filings themselves, registered as Federal Register documents 2026-07988, 07989, and 07990, are the signal. Exchanges file for these protections only when they see patterns in the market suggesting a major liquidity exhaustion event could occur. Additional filings in coming months would indicate the exchanges’ preparation is intensifying.

The 10-year Treasury yield curve. The Federal Reserve sets short-term interest rates directly through its policy rate. The longer-dated end of the Treasury curve, the 10-year and 30-year yields, is determined by the market based on expectations of future inflation, future short rates, credit risk, and foreign demand for U.S. Treasury debt. The Fed influences but does not directly control the long end. Normally it can push long yields lower through quantitative easing (buying long-dated Treasuries to support their prices), through forward guidance (signaling that short rates will stay low), and through the dollar’s reserve currency status (which generates structural foreign demand for Treasuries regardless of yield). When the long end loses anchor, meaning yields rise sharply and refuse to come back down despite Fed jawboning or new asset purchases, the market is pricing in higher inflation, higher risk premium on U.S. debt, or loss of reserve-currency demand. At that point the Fed loses its deepest suppression capability, because the long end is the rate that matters for mortgages, corporate borrowing, and asset valuations broadly. The 10-year yield through the May FOMC minutes and the June Warsh meeting will signal whether the Fed retains its long-end suppression capacity or has lost it. The Warsh Reckoning bear-steepening was a preview of what loss of long-end anchor looks like under a Warsh-led Fed.

Gulf sovereign wealth fund allocation patterns. The Gulf states cannot easily exit dollar exposure because the SWIFT international payment system and the dollar denomination of energy revenue lock them in, but they can rotate within their U.S. holdings between rentier and Genesis-direction names. When the pattern shifts decisively toward Genesis allocations, with more capital flowing to MGX, PIF, and QIA partnerships in defense, energy, and AI infrastructure rather than to traditional U.S. equity funds, the sovereign capital signal is reinforcing the rotation.

Foreign Treasury holdings reported quarterly through the U.S. Treasury TIC (Treasury International Capital) data. Sustained drawdown by China, Japan, and other major foreign holders pressures the Fed’s room to maneuver and accelerates the timeline. Sustained allocation by Gulf SWFs through stablecoin issuers stabilizes the long end and extends the timeline. The TIC data is published with a two-month lag but allows tracking of foreign demand patterns.

Each of these is a smaller signal that confirms or contradicts the bigger Fed posture and insider distribution reads.

Summing

The architecture’s readiness can be tracked. Fed posture indicates whether the institutional alignment is in place. Insider distribution indicates whether the elite positioning is complete. The combined signal indicates whether the trigger event will produce a V-shape rotation or get suppressed before it completes.

None of this signals when. The trigger event depends on Iran kinetic friction, apex earnings cycles, or an exogenous shock. What the tells indicate is whether the architecture is ready when the trigger arrives.

As of this writing in May 2026, both readings indicate ongoing preparation. The Fed posture variable has shifted significantly toward architecture alignment with the Warsh Reckoning of March 2026 and the impending June 16-17 FOMC under Warsh’s chairmanship. Insider distribution velocity remains elevated across both factional categories. The architecture is positioned but not yet staged. The conditions that would tip both indicators toward readiness are accumulating but not yet locked.

The tells signal when the architecture is staged. The trigger signals when the architecture fires. They are different signals on different timelines, and reading both is the difference between watching the chart and reading the architecture.

The money has been moving—Trump tweets have helped insider grifters—but the grift has hidden elite capital rotation (or so called “smart money”—if smart means making john q 401k the bagholders.